Mature and mega VC firms typically don’t place early-stage bets but instead focus on companies that have already achieved some success. In other words, rather than bring new ideas to market and help them grow, these firms prefer to invest in already proven businesses. That’s where micro VCs come in.

Micro VCs are small, nimble firms focused on investing early in companies with high growth potential. Defined as funds smaller than $50- or $100 million, micro VCs play an essential role in financing and incubating new businesses. By taking on more risk, they provide critical funding at a pivotal moment in a company’s development.

By investing in seed and early-stage companies, micro VCs can achieve superior returns. While performance data specific to funds smaller than $100 million is hard to come by, a study of VC performance over 20 years provides some insight.

As Cambridge Associates data shows, return multiples have consistently been significantly higher for smaller funds. In other words, small VC firms have outperformed their larger counterparts. The physics of capital markets would indicate that this should be the case. When firms are small, they generally invest in companies earlier in their development cycle and have more room to grow.

This outperformance is also clearly seen in the net TVPI of new and developing funds by vintage year. The data shows that new and emerging funds are consistently among the top performers.

Further, as Preqin data shows, eight of the ten top-performing venture capital funds have fund sizes of $100 million or less.

Why? There are a few reasons. Beyond the physics of capital markets, smaller firms usually have a different focus and strategy than larger firms. They’re often sector-specific and deeply understand the companies in their domain. Additionally, they tend to be more founder-friendly, providing not just capital but also mentorship and resources. And because they’re often investing alongside angel investors, they’re typically more attuned to the needs of early-stage companies.

Speed is another advantage that micro VCs have over larger firms. They can move quickly to support companies that are gaining traction and need capital to scale. This agility allows them to capture opportunities that others may miss.

Several factors, including the proliferation of technology, the globalization of markets, and the rise of the entrepreneurial economy, have fueled micro VCs.

As technology has lowered the barriers to entry for starting a business, entrepreneurs have more opportunities to bring new ideas to market. At the same time, globalization has created a more level playing field, making it possible for businesses to scale quickly and reach new markets.

This environment is perfect for micro VCs, which are well suited to spotting and backing the most promising companies. And as the number of micro VCs has grown in recent years, so too has the amount of capital available for early-stage companies.

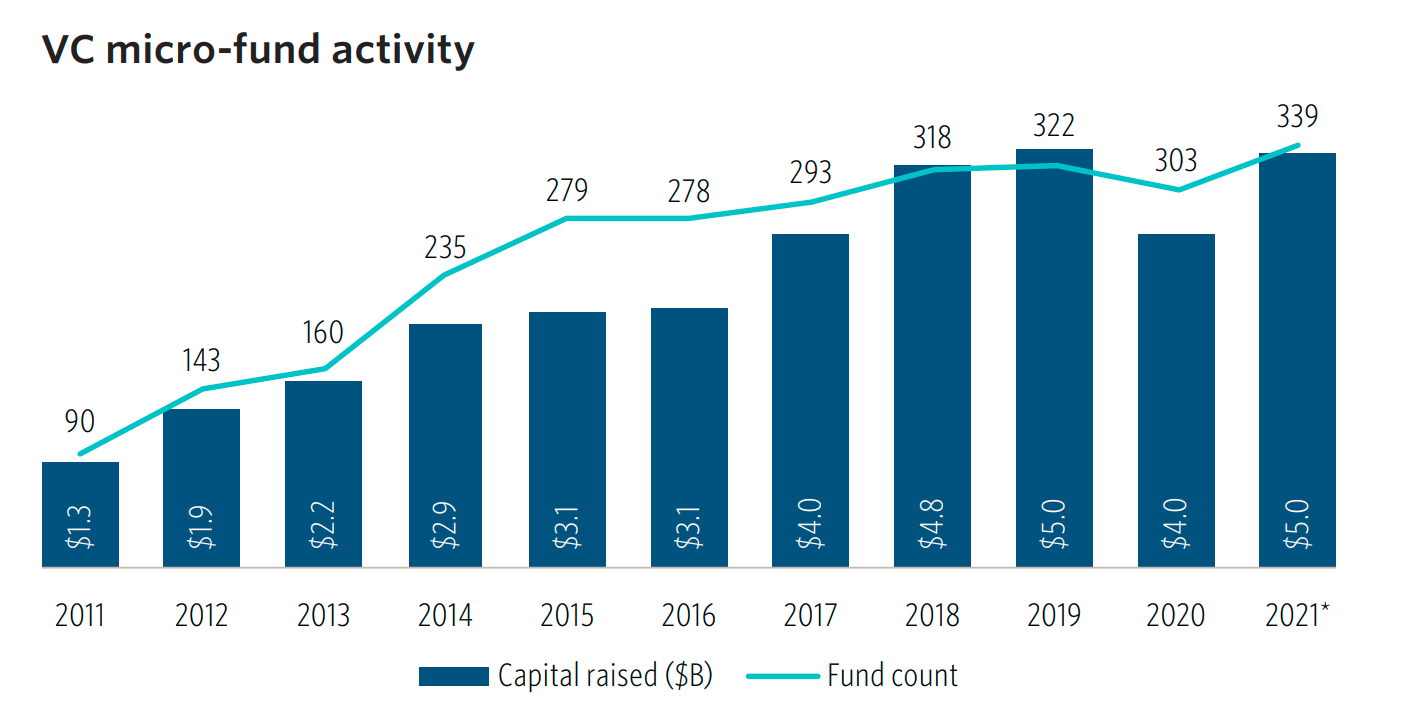

PitchBook data highlights the precipitous rise in the number of micro-funds closed annually, growing “from an average of 75 each year between 2006 and 2011, to an average of 320 each year between 2018 and 2021.”

The AUM of micro VC firms has also exploded, increasing from just over $10 billion in 2011 to over $60 billion in 2021, according to the same PitchBook report.

This growth is driven by several factors, including an increase in LP interest, the rise of new micro VC firms, and the launch of funds focused on early-stage companies. As more capital flows into the space, we’ll likely see even more growth in the coming years.

The rise of micro VC is highly correlated with the rise of seed deals, and seed deals have become increasingly attractive to investors. The most obvious reason is the opportunity for spectacular returns.

In global equities, managers in the top quartile generate an annualized return of around 12.5%, while bottom performers produce 10.7%. In other words, manager selection explains less than 2% of return dispersion. But in private equity, these numbers are grossly different. Some in the bottom quartile of VC funds lose money after inflation, while the top performers return over 30% yearly.

This means that fund selection is a significant driver of outcomes in private equity. To achieve top-quartile performance in private equity, then, it is essential to select the correct fund.

Despite the importance of fund selection, many investors do not have a systematic process for identifying top-quartile performers. This is particularly true for smaller investors who lack the resources to conduct in-depth due diligence on individual managers.

Compounding the challenge, the private equity market has become increasingly crowded and competitive, making it difficult for even experienced investors to identify the best opportunities. In this environment, many investors rely on gut instinct or heuristics when deciding which funds to commit to.

However, several research-based approaches can be used to identify top-quartile performers. One such approach is to seek out emerging managers with a track record of success in other asset classes.

These managers may not have lengthy private equity track records, but they will have deep domain expertise and a proven ability to generate alpha. They will also tend to be nimble and opportunistic, which is often key to success in private equity.

Fund returns decline with fund size, and smaller funds outperform larger funds by 3.65% per year on average. While almost 18% of first-time funds achieve a 25% IRR, later funds only reach that number 12% of the time.

Geographic diversification, too, is an essential factor. Emerging funds can offer exposure to new markets and industries that may be less competitive than traditional private equity markets. Preqin data shows that top-quartile net IRRs at emerging funds were above 20% for 2011-2015 vintages.

In India, small- and mid-cap funds have outperformed large-cap funds by a wide margin. Further, Africa’s VC space is hitting record growth, with exceptionally high funding in areas like crypto.

That said, private equity funds outperform even at the median because they have a key advantage: They can target specific companies and industries rather than being restrained by the need to purchase liquid securities. This allows them to put more money to work on their best ideas and reap the benefits of compounding returns.

Further, a long-term investment horizon enables private equity firms to support a company through thick and thin, which is critical to success in many businesses. In public markets, investors often punish companies for making the investments necessary for long-term growth. In private equity, patient capital provides the time required to make these crucial investments without worrying about short-termism.

For these reasons, private equity should be essential to any diversified investment portfolio. And Gridline makes it easy for individual investors to gain exposure to top-quartile performers in the private equity space. With Gridline, you can access a curated selection of professionally managed alternative investment funds with lower capital minimums, transparent fees, and greater liquidity. So if you’re looking to get the most out of your investments, Gridline is worth checking out.

The S&P 500 recently posted its worst first half in 50 years, and The Fed abruptly ended a bear market rally with the Jackson Hole meeting. Startup prices, too, have plunged. Forge Global, a secondary market, has seen startup prices on its platform drop nearly 20% in February and March compared to the fourth quarter of last year.

In times like these, retail investors tend to sell first and ask questions later, and this time is no different. Venture capitalists are taking a different tack; They’re rushing to buy up depressed assets while they still can, and they’ve already raised the equivalent of two-thirds of last year’s fundraising in the first half of 2022.

The adage is true: when everyone panics, that’s usually the best time to buy. And that’s exactly what VCs are doing.

In the short-term, most economists predict we’ll be entering a recession. While The Fed is attempting a “soft landing,” interest rate hikes have, historically, almost always caused a recession. Moreover, with persistent 40-year-high inflation, rate hikes may be even more painful.

Naturally, this is bad news for asset prices in the short term. A recession means reduced consumer spending, layoffs, corporate bankruptcies, and generally weak economic activity.

That said, venture capitalists have a lengthy time horizon. That’s why, even though the current market conditions may be unfavorable for startups, VCs are still bullish on the long-term prospects of the startup ecosystem.

What’s more, a downturn creates a “shake out” of great talent, which could lead to a surge in the formation of new companies. For example, the dot-com crash of the early 2000s gave birth to some of the most successful companies in recent history, including Google and Amazon.

VCs continue to invest in the face of an impending recession isn’t just a fluke. Research by Neuberger Berman Group shows that private equity funds fared better than public markets in the dot-com bubble and the Great Financial Crisis. Moreover, stocks are more likely to face catastrophic drawdowns during recessions than private companies.

The belief that venture capital is inherently riskier than other asset classes doesn’t bear out in reality. Of course, individual startup investments are indeed incredibly risky. But when you diversify across thousands of companies, such as through a VC fund of funds, the dispersion of returns smooths out, and the risks become more manageable, to the point where VC can be a less risky investment than stocks.

The longer holding period of VC funds allows them to “ride out the storm” and wait for markets to recover. At the same time, a trillion dollars in dry powder is waiting to be deployed in the VC ecosystem, providing a major boost to startup activity in the coming years.

Another tailwind for VCs is implementing the buy-and-build strategy, which has become increasingly popular in recent years. In this strategy, VCs take the opportunity during a downturn to buy up struggling companies at a discount and then integrate them into their portfolio companies. This provides a quick shot of growth for portfolio companies and helps them consolidate their market position.

With Gridline, more investors can access these opportunities and take advantage of the potential stability VC can bring to a portfolio. Further, the SEC’s new ‘accredited investor’ definition opens up these opportunities to a wider range of investors.

In the 2008 recession, seed investing showed continued rapid growth. More recently, private equity firms posted a record $1.4 trillion in dry powder. That’s equal to 100,000 normal-sized deals. Simply put, there’s still plenty of money to go around. This is evidenced not just by continuing investments made by large VCs, such as Drive Capital and Sequoia, but also by the high number of new funds being raised.

So while the current market conditions may be tough for startups, don’t count on VC to dry up. There’s still plenty of money to be made in the startup ecosystem, even in a recession.

It’s no secret that investors are always looking for the next big thing. Whether it’s a new company or technology, they want to be on the ground floor and reap the rewards when it takes off. This is where angel investing and venture capital come in.

Angel investors invest their money in start-ups, usually in exchange for equity. They take on more risk than traditional investors but can also make much more money if the company succeeds.

On the other hand, venture capitalists pool together money from different investors and invest it in early-stage companies. They tend to be more hands-off than angel investors, but they can provide more resources to help a company grow.

Many people see angel investing and venture capital as two sides of the same coin. Both involve taking a risk on a young company, and both can potentially give you a significant return on your investment.

The critical difference is that angel investors are betting on the founder, while venture capitalists are betting on the business. Angel investors tend to invest smaller amounts of money than VCs and are more likely to be involved in the company’s day-to-day operations.

This is because angels invest in the very early stages of a company when the founder is still trying to figure out the business. They’re more likely to invest in a company because they believe in the founder’s vision rather than because they think the business will be successful.

VCs, on the other hand, usually invest later on in a company’s life cycle. They tend to put more money into companies they think have a good chance of becoming profitable.

This doesn’t mean VCs don’t care about the founder’s vision. But they’re more likely to invest in companies with a clear path to profitability rather than those relying on intangibles like the strength of the founder’s relationships or their ability to execute their vision.

Because of this, there are around 300,000 angel investors in the US, compared to fewer than 2,000 VC firms. According to a study by the University of New Hampshire, the average angel deal size in 2020 was $392,025, for 9.6% equity with a deal valuation of $4.1 million. That said, angel deals can be much smaller—even just $15,000 from friends and family.

On the other hand, VC rounds range from a median of $10 million in Series A to mega billion-dollar rounds at later, pre-IPO stages.

Many investors choose to invest in both angels and VCs. This can be an excellent way to diversify your portfolio and expose you to different stages of a company’s life cycle.

If you’re investing in VCs, you usually invest in later-stage companies with a higher chance of success. But this also means you’re missing out on the potential upside of investing in a new start-up.

Angel investing can give you access to start-ups that might not be able to get funding from VCs. And because you’re investing in the very early stages of a company, you can make a much larger return if the company is successful.

Of course, there’s also more risk involved with angel investing. You could end up losing your entire investment if the company fails. But for many investors, the potential rewards are worth the risk.

There are a few reasons why it makes sense to invest in both angels and VCs:

Of course, some risks are also to consider before investing in angels or VCs. But for many investors, the potential rewards outweigh the risks.

To gain exposure to these earlier-stage companies and reap the potential rewards, consider investing via Gridline. As a digital wealth platform, Gridline provides access to a curated selection of professionally managed alternative investment funds with lower capital minimums, fees, and greater liquidity. You can build a diversified portfolio of private market assets more efficiently.

As recession fears mount, the tech industry has been especially hard hit. The war in Ukraine, 40-year highs in inflation, and an interest rate turnaround are all taking their toll. The industry is now bracing for a historic slump, with VC firms pulling back, layoffs looming, and share prices plummeting.

For the past few years, the industry has been on a tear, with companies like Apple, Amazon, and Google seemingly invincible. But now, those same companies are facing serious headwinds.

Apple, for example, is down $500 billion from its peak market value in January, despite posting record revenue. Microsoft, Amazon, Tesla, and Alphabet have all lost more than 20 percent of their value this year, while Netflix has lost a staggering 70 percent.

Another notable casualty has been Facebook, which is down 40 percent this year. The social media giant recently announced that it would freeze hiring, and it’s not the only one cutting back on costs.

Start-ups have also been hit hard, with around 30 companies laying off employees since the beginning of April, according to Layoffs.fyi, which tracks layoffs in the tech industry.

With major companies shedding talent, skilled workers are increasingly striking out on their own. This “shake out” of great talent could lead to a surge in innovative new startups over the next few years.

For early-stage investors, this presents a unique opportunity to get in on the ground floor of some potentially groundbreaking companies. In other words, a “dip” in the market may actually be a great time to invest in the next generation of tech companies.

Similar to public markets, private markets experience a decrease in value during an economic recession.

This VC pullback can have a big impact on startup funding. When VCs are less active, it can lead to lower valuations and fewer rounds of financing for startups. As a result, many startups are forced to scale back their operations or even shut down entirely.

One major VC slump was during the dot-com crash of the early 2000s. This downturn led to the demise of many multi-billion-dollar startups, including Pets.com and Webvan.

However, the dot-com crash also gave birth to some of today’s most successful companies, such as Google and Amazon. So while a VC pullback can be devastating for some startups, it can also create opportunities for others to thrive.

Moreover, VC pullbacks are neither as deep nor as prolonged as public market slumps. Research by Neuberger Berman Group highlights that private equity funds fared better than public markets in the dot-com bubble and the Great Financial Crisis.

If you’re thinking about investing in tech startups, the current market conditions may actually be in your favor. With VC activity down, startups are more likely to be open to accepting financing at lower valuations. This means you can get in on some potentially great companies at a discount.

Of course, it’s important to do your homework before investing in any startup. But if you’re patient and pick your investments carefully, the current market conditions could be a great opportunity to score some big wins in the years to come.

Diversification is key, and Gridline’s platform enables access for individual investors to gain diversified exposure to non-public assets – crucial in today’s market landscape.

The common notion is that to make money in venture capital, you must take on a lot of risk. After all, the dispersion of returns is far higher in VC than in other asset classes, which means that the risk of selecting a poorly performing investment is also higher.

The apparent instinct is to increase the size of the venture fund to reduce the risk of individual investments, but that’s not always the right move. Larger funds consistently underperform smaller ones, and established managers underperform emerging ones.

The trick is not to invest in larger funds but in many different funds across sectors, geographies, and stages. By investing in a wide variety of VC funds, you can offset the risk of any individual investment while still participating in the potential upside of the asset class.

The main reason that investing in multiple VC funds reduces risk is that it leads to more investments, and more investments lead to lower dispersion of returns.

An Institutional Investor report simulated two VC portfolios: One with 15 investments and another with 500 investments. They found that the former yielded a median return of around 10 percent, with bottom-quartile funds losing money and the top-quartile funds experiencing large internal dispersion.

In contrast, the 500-deal fund experienced 10 to 17 percent returns, similar in size to that of public equity funds. But, with proper diversification, it’s possible to achieve a reasonably safe, predictable return profile in venture capital while outperforming public markets.

Similar to how Vanguard introduced the concept of index funds to reduce the risk of investing in stocks, you can also reduce your risk by reducing the number of bets you’re making on any particular VC fund. Today, index funds are a popular way to invest in stocks, like the S&P500 and Dow Jones Industrial Average, and there are ways to do the same with VC.

Research finds that two-thirds of venture capital deals fail, meaning a VC’s ending portfolio size is one-third of its invested companies. Since classical portfolio theory suggests investing in 20-30 equities at once, with more recent research suggesting 40-70 investments, a well-diversified portfolio would include from 60 to 210 investments.

The problem is that very few VC funds have this many investments. The typical VC fund is concentrated in <20 to 40 deals, which is too small to provide the kind of diversification that would offset the risk of individual investments.

The solution, then, is to commit to many different VC funds. The problem with this, however, is that minimum investment sizes quickly add up, making it impossible for everyone but the most deep-pocketed investors to participate.

The better solution is to find a way to invest in many different VC funds without having to commit large sums of money. With Gridline, for example, you can deploy $100,000 across ten different funds, each making 30 investments. This gives you the diversification of 300 investments, equivalent to just $333 per investment.

With a portfolio like this, you can offset the risk of any individual investment while still participating in the potential upside of the asset class. And best of all, you can do it without committing large sums of money.

Systematic vetting of funds can help ensure that you are more likely to select above-average managers. An experienced advisor and/or a platform like Gridline will run a comprehensive due diligence process that digs into granular details of the fund’s operations, legal structure, compensation structure, regulatory compliance, and reliance on third-party service providers.

Generating above-average, risk-adjusted returns in these markets comes from investing in a variety of diversified well-vetted top-tier fund managers.

Few industries have been as tribal and opaque as venture capital. For years, the VC world was a mystery to outsiders, with its language and customs. But in recent years, there has been a growing effort to make the industry more transparent.

A recent study published by the National Bureau of Economic Research (NBER) sheds new light on how VC fund of funds outperform the market and reduce risk. The study found that the average VC fund of funds generated net returns that outperformed the S&P 500 and Russell 2000 PMEs.

Today’s stock market is in a record bull run, but that doesn’t mean there aren’t risks. Many experts believe we are overdue for a market correction.

After all, periods of exuberance in public markets are punctuated by years of lethargy as performance reverts to the mean. For instance, in the decade after the dot-com crash, the PME index annual return dropped to 0.08%, while private equity maintained a 7.5% average.

This is because VCs are more likely to invest in companies with high potential growth. As the NBER study confirms, company-level returns within a specific VC fund follow Pareto’s Principle: 20 percent of the companies within a fund generate 80 percent of returns.

In other words, VCs are more likely to generate returns by investing in a small number of high-growth companies. This is why VC funds outperform the market during bull markets and experience less severe corrections during bear markets.

Moreover, it’s not just top-quartile VC funds that outperform the market. The NBER study found that “VC funds in the 2nd quartile also have PMEs above 1.0, overall and for both pre-2001 and post-2000 vintages.” This means that, on average, you are better off investing in a mediocre VC fund than a publicly-traded market index.

The premise of diversification is simple: don’t put all your eggs in one basket. And yet, many investors still don’t diversify their portfolios enough.

One way to diversify is to invest in a VC fund of funds. These investment vehicles invest in various VC funds, reducing the risk of any fund underperforming.

The NBER study found that the average VC fund of funds outperformed the market by a wide margin. Not only have buyouts “consistently outperformed public markets with the average PME being 1.20 across the sample,” but “VC funds, overall, also have out-performed public markets with the average PME of 1.22 across the sample.”

This is likely because these vehicles have access to a large pool of capital and can invest in more companies than most individual investors.

In addition, VC fund of funds are more likely to generate returns by investing in a small number of high-growth companies. VC investing is risky at the company level, but it is lucrative at the portfolio level.

The NBER study reiterates what many experts have long known: venture capital is a smart investment strategy for those who can stomach the risk. For those who want to reduce their risk, investing in a VC fund of funds is an ideal way to diversify your portfolio and get exposure to the top performers in the industry.

But what about the average investor? Can they still benefit from this strategy? The answer is a resounding yes. With a Gridline Thematic Portfolio product, you can invest in 5 to 10 institutional-grade VC funds for just $100,000. This allows you to achieve the same level of diversification and exposure to top performers as the wealthiest individuals and endowments.

So don’t miss out on this opportunity to supercharge your portfolio. Invest in a VC fund of funds today.

As an investor, you always seek ways to protect your portfolio from volatility and market downturns. One way to do this is by diversifying your investments into assets that don’t move in lockstep with the stock market.

These so-called “non-correlated assets” include private equity, real estate, and venture capital. While these investments may be riskier than traditional stocks and bonds, they can offer a hedge against market volatility.

More accurately, they might be called “less-correlated assets.” That’s because they may not always move in the same direction as the stock market; they’re still subject to the same economic forces.

One example illustrating alternative asset benefits is the dot-com bust of the early 2000s.

While the stock market plunged, certain alternative investments held up relatively well. For instance, private equity firms continued to make money by investing in companies out of favor with the public markets.

As Bain describes, “in the decade following the dot-com crash, the PME index’s annual return fell to 0.08%, while private equity maintained a 7.5% average.” So, while the stock market struggled to recover, private equity was still generating returns for investors.

Gold is often seen as a safe haven asset to park your money when the stock market is in turmoil.

Its low correlation to other asset classes makes it an ideal diversification tool. EquityZen writes that it correlated just 0.23 to the overall market between 2006 and 2015. The correlation is even lower in 2022, with a 14% correlation to the high-growth benchmark, ARKK.

And when the stock market is struggling, gold typically shines. For instance, gold prices soared when the stock market crashed in 2008.

Even less correlated to public markets is venture capital. VC is the investment of money in a new business venture, usually in the form of equity. It’s a high-risk, high-reward asset class, but it can offer big returns for investors.

According to an Invesco white paper, VC correlates -0.06 to large caps in the public markets. That means it’s uncorrelated or even slightly negatively correlated.

This makes sense when you think about it. After all, VC is investing in companies that are often too small or too new to be publicly traded. So, while the stock market may be struggling, VC can still be going strong. AngelList reaffirms these findings with an analysis of its data. It found a correlation of 0.0 between the gross monthly change in AngelList’s seed portfolio and the Nasdaq Index.

You need to invest in top-tier, actively managed VC funds to benefit from this. But these have high minimum investment requirements, often $500,000 or more.

For the average individual investor, this can be out of reach. Gridline offers a solution with its Thematic Portfolio products, which invest in 5-10 institutional grade VC funds. These have minimum investment requirements of just $100,000.

The debate around whether digital assets are correlated or uncorrelated to the stock market is ongoing. Fueling the uncertainty is the highly-volatile nature of the asset class.

However, a Nasdaq article points out that, in 2021, the peak 90-day correlation between Bitcoin and the S&P 500 was a mere 0.31, with a low of -0.04 in June 2021.

Further, altcoins can have an even lower correlation with the stock market. While these assets themselves are highly volatile, a small allocation to them could help reduce the overall volatility of a portfolio.

Alternative assets can offer a hedge against market volatility and downturns. They may be riskier than traditional investments, but they can offer higher returns and greater diversification. So, if you’re looking to protect your portfolio from the ups and downs of the stock market, consider investing in some alternative assets.

With the Federal Reserve raising interest rates for the first time since 2018, many investors are wondering how this will affect their portfolios. While higher rates can mean higher borrowing costs and increased volatility in the stock market, they can also lead to higher returns on certain investments.

Here’s what investors need to know about rising interest rates.

Rising interest rates can lead to increased volatility in the stock market. This is because when rates rise, it becomes more expensive for companies to borrow money. As a result, stock prices may fall as investors worry about the impact of higher rates on corporate profits.

This held true in the recent interest rate hike, with the Nasdaq 100 entering correction territory. Previously, low rates, and thus low bond yields, drove investors into riskier assets, which helped contribute to the outperformance of the S&P 500 in 2020 and 2021. This time around though, with rates on the rise, we’re seeing investors move out of stocks.

While rising interest rates can be bad news for the stock market overall, there are some sectors that actually benefit from higher rates.

For example, banks and other financial institutions tend to do well when rates rise because they can charge higher interest rates on loans. This includes the likes of banks, brokers, and insurance stocks.

Further, as a rising interest rate environment is associated with a strong economy, certain sectors like industrials and consumer discretionary stocks may also outperform. This is because improved employment and a healthier housing market lead to greater spending on big-ticket items.

Blue-chip investors looking for higher returns may also benefit from rising interest rates. For instance, short-term and medium-term bonds are less sensitive to rate increases.

2021 was an unprecedented year for private markets, with record-breaking inflows into venture capital. This was in part due to the low interest rate environment, as investors were seeking higher returns than they could get in the stock market or in bonds.

Now that rates are on the rise, we may see venture capitalists start to pull back on their investments. This could lead to a slowdown in the growth of private companies and a drop in the valuations of venture-backed companies.

That said, the impact likely wouldn’t be too severe. For instance, research from the European Financial Management Association showed that a 1% increase in interest rates “reduced venture capital fundraising by $647 million the following year—or about 3.2%.” While this doesn’t include the longer-term effects of higher rates, it does show that the impact of rising rates on venture capital isn’t as acute as some may think.

Given the potential impact of rising interest rates on investments, it’s important for investors to review their portfolios and make sure they are properly diversified. This means having a mix of investments that will perform well in different market conditions.

While there’s no guarantee that anything will outperform in a rising rate environment, by diversifying your portfolio and having a long-term investment plan, you’ll be in a better position to weather any market changes.

Gridline is a digital wealth platform that provides a curated selection of professionally managed alternative investment funds and enables access for individual investors, and their advisors, to gain diversified exposure to non-public assets with lower capital minimums, lower fees and greater liquidity.